Mar 10, 2026

May 15, 2026

5 Mins Read

Table Of Content

Related Articles

SMS Bombing

Dark Web Monitoring

Feb 19, 2026

Threat Actors

Jan 08, 2026

Dark Web

Jan 31, 2026

Ransomware

Jan 31, 2026

What is Carding Fraud?

Carding fraud is the unauthorized use of stolen payment card data to make purchases or verify card validity. Card testing is a core part of how it works: automated bots run small or zero-value transactions against a merchant’s checkout to confirm which stolen card numbers are still active. In 2026, carding is driven almost entirely by automation. Detection speed and response quality are what separate merchants who contain the damage from those who absorb it.

What is Carding?

Carding begins when fraudsters acquire stolen card data, usually from dark web marketplaces or breach databases. They load thousands of card numbers into automated tools and fire them at real checkout pages. A successful charge, even a $0.01 one, confirms the card is live and ready to be sold or used for larger purchases. The merchant absorbs the chargeback. The fraudster moves on.

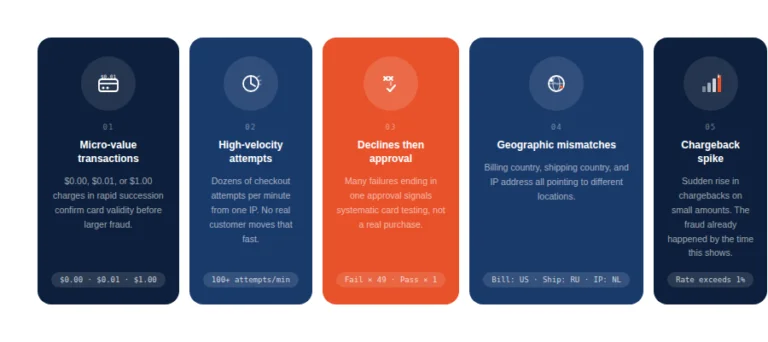

Identification: 5 Early Warning Signals

Spotting carding activity early limits financial exposure and chargeback penalties.

- Unusual volume of small or zero-value transactions

Charges of $0.00, $0.01, or $1.00 appearing in quick succession are a classic card testing signature. Fraudsters use minimal charges to confirm card validity before attempting larger purchases elsewhere.

- High-velocity transactions from a single IP or device

Bot-driven checkout spikes produce transaction patterns no human user could replicate. Multiple attempts within seconds from the same origin point to automation, not a real customer.

- Sequential declines followed by an approval

A series of failures across different card numbers ending in one approval indicates systematic card testing rather than normal checkout behavior.

- Geographic mismatches

Billing addresses in one country, shipping addresses in another, or orders from IP addresses that do not match the card’s issuing region are common carding attack indicators.

- Elevated chargeback rates in a short window

A sudden spike in chargebacks, especially for small amounts, often follows a carding wave that went undetected during testing.

Incident Response: Mitigation in Under 60 Minutes

When carding activity is confirmed, a fast carding incident response plan limits damage.

- Block identified IP ranges or device fingerprints generating suspicious traffic. This stops the active bot session without touching legitimate users.

- Enable or tighten rate limiting and CAPTCHA on the checkout page. Together they raise the cost of automated testing significantly.

- Activate BIN attack blocking if traffic clusters around a specific Bank Identification Number range. This stops fraudsters from cycling sequential card numbers.

- Notify your payment processor immediately. They can apply additional verification layers and assist with chargeback disputes.

- Document the incident with timestamps, transaction IDs, IP data, and device fingerprints for compliance and potential law enforcement use.

Advanced Prevention: Behavioral Biometrics and the 2026 Fraud Stack

Legacy tools use static rules and velocity checks. These are necessary but no longer sufficient against modern bots.

| Legacy Approach | 2026 AI-Driven Approach |

| Rule-based velocity limits | Behavioral analytics for fraud detecting anomalous session patterns |

| Simple CAPTCHA | Agentic AI fraud detection adapting to bot behavior in real time |

| Manual review queues | Automated risk scoring with real-time intervention |

| Address verification only | 3D Secure 2.3 with biometric and behavioral signals |

3D Secure 2.3 adds richer authentication signals, including device data and transaction history. It reduces friction for real customers while raising the bar for fraudsters. It does not eliminate card-not-present (CNP) fraud entirely, but it makes carding attacks considerably more expensive to run.

The Cost of Inaction: Business and Compliance Impact

Unchecked carding creates compounding costs. Chargeback fees accumulate on every fraudulent transaction. Exceeding processor thresholds risks merchant account suspension. Card brands can impose fines and remediation requirements under PCI DSS compliance 2026 standards. Beyond direct losses, a publicized fraud incident damages customer trust and conversion rates.

Merchant account protection requires treating carding as an ongoing operational risk rather than a periodic problem.

FAQs

What is the difference between carding and card cracking in 2026?

Carding uses stolen card data to make transactions. Card cracking involves obtaining partial card details and using brute force or social engineering to fill in the missing information.

How do I identify a bot-driven carding attack in real-time?

Watch for the five signals above, particularly velocity anomalies and zero or micro-value transactions. Real-time fraud scoring tools surface these patterns automatically.

Why is my checkout being used for $0.00 or $1.00 transactions?

These are card testing attempts. Fraudsters confirm card validity with a minimal charge before using the card for high-value fraud elsewhere.

Can carding fraud lead to my merchant account being suspended?

Yes. Excessive chargebacks and fraud rates trigger processor reviews that can result in suspension or termination of your merchant account.

How does agentic AI help prevent automated card testing?

Agentic AI systems monitor session behavior continuously, identify bot patterns that static rules miss, and adjust response thresholds dynamically based on observed activity.

What are the most common carding attack indicators for e-commerce sites?

Unusual transaction velocity, micro-value charges, mismatched billing and shipping geographies, and sequential decline-then-approval patterns.

Will 3D Secure 2.3 eliminate card-not-present fraud risk?

No. 3D Secure 2.3 substantially reduces CNP fraud risk by adding authentication friction and richer signals, but determined attackers continue to find workarounds, particularly as AI tools improve.