Jul 31, 2026

Feb 26, 2026

9 Mins Read

Jul 08, 2026

Finance Industry Under Pressure: What U.S. Institutions Need to Know in 2026

The digital transformation of the financial industry has revolutionized how we bank and trade, but it has also afforded cybercriminals unprecedented opportunities to exploit the vast scale and speed of modern finance. Today, the United States financial system stands squarely at the center of the global cybercrime economy, enduring roughly half of all financial phishing attacks and nearly a quarter of all dark web threat activity.

As adversaries pivot from basic software exploits to highly sophisticated, AI-driven crime waves, relentless Business Email Compromise (BEC) campaigns, and stealthy third-party supply chain infiltrations, the stakes have never been higher.

This post breaks down why the U.S. financial sector is uniquely in the crosshairs, explores the dominant attack vectors defining today’s threat landscape, and provides actionable, back-to-basics strategies for financial leaders to fortify their defenses against an increasingly unpredictable adversary.

Why is the U.S. financial sector uniquely in the crosshairs of cybercriminals?

The United States financial sector is the primary global hotspot for cyber threats, accounting for 23.52% of all finance-related dark web threat activity and a staggering 48.02% of global phishing activity. This unique position as a primary target is driven by several intersecting factors:

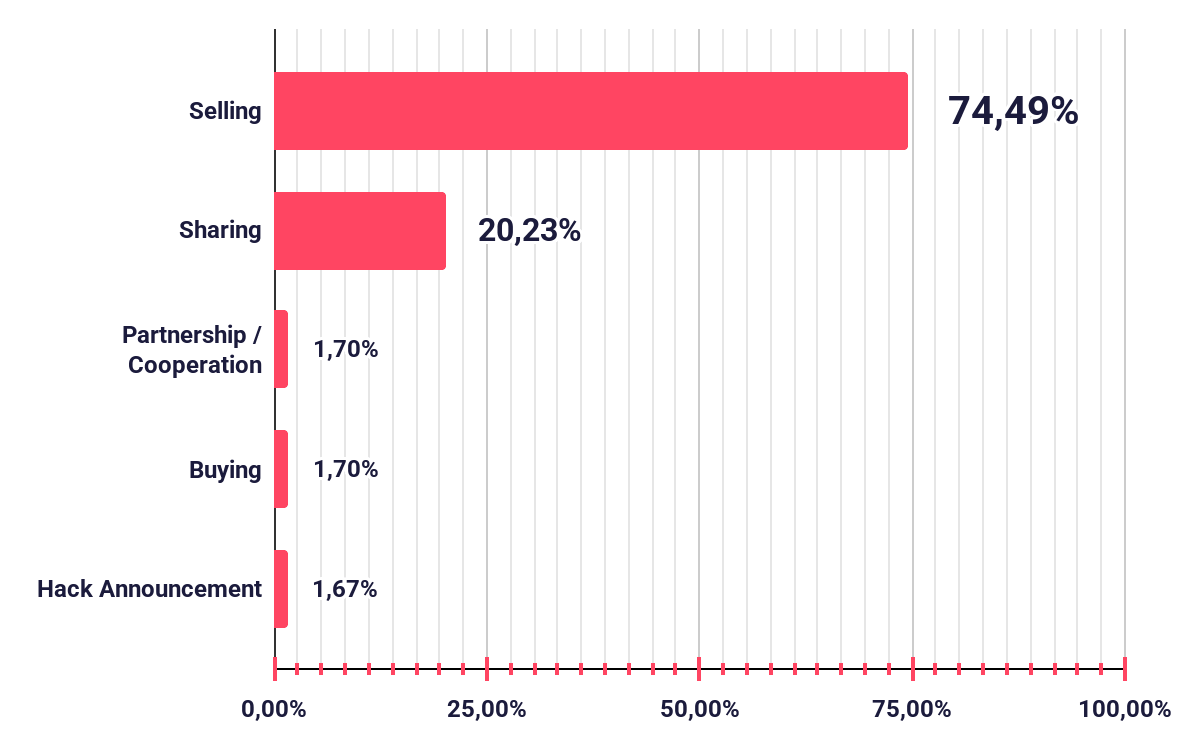

Massive Market Size and High-Value Data: The sheer scale of the U.S. financial market, combined with its mature digital infrastructure, makes it highly lucrative. Cyber threats against the sector are overwhelmingly driven by monetization, with over 80% of dark web threat types centered on exposing data and databases. Threat actors prioritize stealing valuable customer records, account details, and internal financial datasets, which they then trade in underground markets, as evidenced by the fact that 74.49% of dark web posts involve selling these assets.

Distribution of Dark Web Threats by Threat Categories – Finance Threat Landscape Report

Rapid Digital Transformation and Real-Time Payments: The accelerated shift to digital banking has given criminals unprecedented opportunities to exploit the high speed and vast transaction volumes of modern finance. The growth of real-time payment channels has introduced new vulnerabilities, challenging banks and payment processors to defend against faster, more complex fraud schemes.

Targeting by Foreign State-Sponsored Actors: The U.S. financial system is heavily targeted by sophisticated cybercriminal organizations and nation-state actors. For example, the sector faces direct threats from North Korean IT workers who use fraudulent identities to gain employment within U.S. company networks. Once inside, these operatives exfiltrate proprietary data, facilitate cybercrimes, and generate illicit revenue for their regime.

What are the dominant attack vectors targeting U.S. financial institutions?

Social Engineering and Business Email Compromise (BEC): BEC and social engineering are among the most financially damaging and consistent attack vectors, driving roughly half of all cyber claims in recent years. Rather than relying solely on software exploits, attackers utilize sophisticated phishing, smishing (SMS), and vishing (voice) campaigns to deceive employees and bypass security protocols.

Advanced groups, such as Scattered Spider, have successfully social-engineered IT help desk employees into resetting passwords, enabling them to gain unauthorized access and deploy disruptive malware.

AI-Powered Exploits and Deepfakes: The rapid advancement of Generative AI has provided cybercriminals with new tools to scale and perfect their attacks.

- Enhanced Phishing and Spoofing: Attackers use AI to generate flawless phishing emails, realistic voice clones, and deepfake videos to bypass biometric authentication systems and execute highly convincing imposter scams.

- Malicious LLMs: Cybercriminals leverage weaponized Large Language Models (LLMs) to automate malware creation and discover system vulnerabilities.

Ransomware and Double Extortion: Ransomware operators continue to heavily target the financial industry. These groups typically gain initial access via phishing campaigns or by exploiting vulnerable infrastructure. Once inside, they frequently utilize a “double extortion” strategy: exfiltrating highly sensitive financial data before encrypting the network, and demanding a ransom both to restore operations and to prevent the public release of the stolen data.

Fraudulent Remote IT Workers (Insider Threats): A highly concerning and stealthy attack vector involves foreign state-sponsored operatives, notably North Korean IT workers, infiltrating corporate networks disguised as remote employees. Using stolen identities, fabricated resumes, and “laptop farms” to bypass geographic restrictions, these actors secure remote IT positions within U.S. companies. Once hired, they leverage their legitimate internal access to install backdoors, log keystrokes, exfiltrate proprietary data, and generate illicit revenue for their regimes.

Zero-Day Vulnerabilities and Supply Chain Attacks: Advanced Persistent Threat (APT) groups and sophisticated hackers can weaponize undiscovered “0-day” vulnerabilities in operating systems, network infrastructure, and enterprise software to bypass defenses for extended periods. Because financial institutions rely on complex networks of third-party vendors, attackers can also execute supply chain attacks. By compromising a weaker vendor, attackers can persistently infiltrate the broader financial supply chain.

Mobile Device Exploitation and Account Takeover (ATO): Financial institutions’ reliance on mobile banking applications has made mobile devices a critical single point of failure. Cybercriminals deploy specialized mobile trojans, spyware, and zero-click attacks to compromise devices. They heavily utilize SIM hijacking and OTP (One-Time-Password) bots to intercept authentication codes. These tactics allow attackers to fully bypass multi-factor authentication, seize control of customer accounts, and drain funds. You can check our research, Industrialized Social Engineering: Deep Dive Into the OTP Bot Ecosystem for more information.

What role do third-party vendors play in terms of risk?

Third-party vendors act as critical vectors for systemic risk, primarily serving as weak links that allow threat actors to scale their attacks and infiltrate multiple downstream organizations simultaneously. Their role in elevating systemic risk is characterized by several key vulnerabilities:

Conduits for Massive Supply Chain Attacks: Cybercriminals and APT groups frequently compromise the internet-facing systems of third-party software providers to gain persistent access to a wider network of targets. For instance, the XE Group exploited zero-day vulnerabilities in a supply chain management software for information theft.

Exploitation of Contracted IT Services: Outsourced IT and helpdesk vendors are prime targets for sophisticated social engineering. The cybercriminal network Scattered Spider successfully breached a major international company by deceiving the employees of its contracted IT service desk. This vendor compromise allowed the attackers to deploy highly disruptive malware, highlighting the cascading financial damage of third-party risk. The victim company ultimately sought $380 million in damages from the IT provider.

Vulnerabilities in Verification and Onboarding: Organizations increasingly rely on third-party vendors for identity verification when hiring remote IT workers or for other purposes. If a third-party vendor’s verification processes are flawed, organizations face the systemic risk of unwittingly hiring fraudulent remote workers such as foreign state-sponsored operatives who use fake identities to infiltrate networks.

Conclusion

The cyber threat landscape facing the U.S. financial sector has fundamentally shifted from opportunistic technical experimentation to a highly professionalized, monetization-driven ecosystem. Today’s adversaries operate with unprecedented speed and scale, leveraging everything from 0-day vulnerabilities and weaponized Generative AI to sophisticated social engineering and fraudulent remote IT worker schemes.

It is clear that threat actors are no longer just trying to breach the vault; they are targeting the very foundation of modern banking. They are after the databases, which now account for nearly 81% of all finance-related dark web threat activity. Furthermore, as financial institutions increasingly rely on artificial intelligence for everything, these AI models themselves have become prime targets for manipulation, data poisoning, and evasion.

Defending against this AI-induced crime wave requires an immediate departure from reactive, purely rule-based security and slow processes. Financial institutions must adopt a proactive defense strategy that can dynamically adapt to emerging threats. Yet, technology alone is not a silver bullet. As the devastating success of social engineering attacks demonstrates, the most sophisticated attacks often succeed by exploiting basic human and procedural gaps.

To survive this escalating arms race, organizations must combine advanced threat intelligence with rigorous operational discipline. The path forward requires a unified approach that hardens both digital infrastructure and the human firewall.

What Actions Should U.S. Financial Leaders Take?

- Mandate MFA: Require Multi-Factor Authentication (MFA) for all remote access and email systems. Prioritize hardware tokens or app-based authenticators over SMS text messages, which are highly vulnerable to interception.

- Enforce Out-of-Band Authentication (OOBA): Do not treat OOBA as just a guideline; make it a strict, formal requirement embedded into financial operations. Always verify sensitive requests, such as wire transfers or changes to payment details, through an independent communication channel, like calling a known, pre-established phone number.

- Maintain Rigorous Patching and Vulnerability Management: Execute a proactive vulnerability management program to quickly patch critical flaws, particularly in internet-facing edge devices like VPNs. Ensure you have a strategy to manage and replace aging, End-of-Life (EOL) IT assets, as prolonged use of legacy systems introduces major security vulnerabilities.

- Back Up Data and Segment Networks: Defend against ransomware by maintaining reliable, secure data backups and segmenting your networks so that a breach in one department cannot easily spread to critical financial databases.

- Establish Tested Incident Response Plans: Develop and regularly test disaster recovery and business continuity plans to ensure your institution can maintain operations and recover swiftly during a cyber crisis.

- Conduct Regular Phishing and Security Training: Invest heavily in employee education and phishing simulations to help staff recognize sophisticated business email compromise (BEC) and social engineering attempts. Staff responsible for handling payments should be retrained at least annually.

- Implement Strict Remote Hiring Verification: To prevent the infiltration of fraudulent remote IT workers, train HR to spot basic red flags such as a candidate’s strong reluctance to do a video interview and rely on robust, potentially AI-assisted identity verification processes.

- Monitor the Dark Web: Utilize Dark Web Monitoring services to rapidly detect if your company’s data, customer records, or employee credentials have been exposed in underground markets.

- Audit AI and Keep Human Oversight: If your institution uses AI for trading or risk modeling, regularly audit the training data to eliminate “poisoned” or manipulated inputs. Always keep human supervision in the loop to ensure AI does not autonomously trigger irreversible financial disruptions.

Table Of Content

Related Articles

Top 10 MSSPs in Belgium (2026)

Cyber Risks for Wearable Technologies

Jul 27, 2026

Top 10 MSSPs in the UK in 2026

Jul 17, 2026

SOCRadar XTI Is Live on the Chrome Web Store

Jul 16, 2026